In brief: what the data says

- Latin America is a small buyer in a big, concentrated market. The region is home to about 8% of the world's people but accounts for only around 5% of a roughly US$1.7-trillion global pharmaceutical market, while the United States alone takes about 53%.2 In the active ingredients that underpin every medicine, the region holds less than 1% of global production capacity.3

- Capacity is not the same as autonomy. LAC factories already supply the majority of the medicine the region physically consumes (about 73% of finished-medicine volume in Brazil, roughly 80% in Colombia, around 70% in Argentina, and about 60% of Cuba's essential-medicines list),4 yet the region still imports about 91% of its medicine value from outside LAC (ECLAC, measuring intra-regional trade independently, puts the extra-regional share at about 87%).

- The exposure is high-value, not high-volume. LAC imports 91% of its medicine value but only about 53% of the kilograms it buys; extra-regional medicines cost roughly US$103 per kilogram against about US$12 for intra-regional ones,5 so a supply shock bites hardest in the complex, patented drugs that get export-restricted first.

- It runs deeper than finished drugs, into active ingredients. Even the regional producers import about 59% of their active ingredients (by value) from China and India; Brazil now makes only about 5% of its own, down from roughly 55% in the 1980s.1 The rest of that supply is mostly European and US, not regional, so the dependency is deeper than the China-and-India figure alone suggests.

- Genuine export capacity is almost absent. Of all 33 countries, only the Dominican Republic shows a real export edge, and it is a US-facing free-zone enclave, not capacity the region could redirect to its own shelves in a crisis. Almost no country holds spare, exportable capacity to share.

- The pieces of a regional answer exist; a region-wide vehicle does not. Pooled procurement has saved Central America's COMISCA bloc on the order of US$210 million and cut prices 30–60% across many products;6 paired with selective production, coordination could repatriate 19–32 points of dependence by 2035, on the order of US$8–13 billion a year.7 But the region still has no single integration tool, so the work is to build one from a willing few.

- We cannot fully manage what we cannot measure. No standardized, region-wide series exists for how much of each country's medicine demand is met by domestic production. Building that visibility is itself one of the cheapest, fastest moves available, and a precondition for steering the rest.

The verdict. Latin America and the Caribbean already make most of their own medicines by volume: the region's factories supply the majority of the pills its people take. The supply-security gap is therefore narrower, and more specific, than the familiar "the region cannot make its own medicines" worry. It sits in two places: the high-value, patented drugs, and the active ingredients behind nearly all medicines, about 59% of which the region buys from China and India.1 That gap is worth on the order of US$33 billion a year in imported medicine value, a conservative floor: the ten largest markets alone source about US$29 billion of their medicine from outside the region. Closing it is not a choice between building 33 national factories and importing everything; it is a regional question with several levers at once, and the region is already piloting every one of them. The opportunity is to do them on purpose, and together.

How to read this report: we measure dependency in dollars and active ingredients, not factory counts

A debate that turns on "does the region make its own medicines?" usually gets answered with anecdotes: a vaccine plant here, a generics champion there. We measured the dependency directly instead, in two currencies that matter for supply security, money and molecules.

For finished medicines we used United Nations Comtrade trade data (HS chapter 30) for all 33 LAC countries, computing each country's share of imports sourced outside the region by summing its imports from every Latin American and Caribbean partner against its world total: an all-partner method, not a top-handful approximation, run by both value and net weight in kilograms.

For active pharmaceutical ingredients we used the EFPIA-curated basket of HS6 codes that isolates pharmaceutical-use ingredients, and traced their origin. To locate genuine production capability we computed each country's revealed comparative advantage in pharmaceutical exports, and to size the opportunity we built a transparent scenario model to 2035. Where the data thins we say so: robust production-volume statistics exist for only about eight to ten of the 33 countries, five (Cuba, Haiti, Venezuela, Saint Lucia, Saint Kitts and Nevis) do not report recent trade, and the headline number is deliberately a lower bound.

Latin America sits at the margin of a US$1.7-trillion industry, buying far more than it makes

To understand the region's exposure, start with where it sits in the world. The global pharmaceutical market is worth roughly US$1.7 trillion a year, and it is extraordinarily concentrated: the United States alone accounts for about 53% of it.2 Latin America and the Caribbean, 33 countries and roughly 8% of the world's population, accounts for only about 5%, on the order of US$92 billion.2 The region consumes far more medicine than its market share suggests it should, and it makes far less.

The asymmetry is starker one layer down, in the active pharmaceutical ingredients (APIs) that are the molecular starting point of every drug. Global API manufacturing is dominated by two countries: India and China together hold roughly two-thirds of registered production capacity, and Latin America and the Caribbean accounts for less than 1% of it.3

This is the global backdrop against which the rest of this report should be read. When LAC's dependence on China and India comes up later, it is tempting to assume the remainder is made at home. It is not. The region is a small, late entrant in a market where a handful of countries make the active ingredients and most of the world, rich and poor alike, buys them. LAC's particular challenge is not that it is uniquely dependent; it is that it has the least capacity of any major region to do anything about it when supply tightens.

The burning platform: in 2020 the region learned that capacity on paper is not supply when the world closes its doors

In the first months of the COVID-19 pandemic, the abstract idea of "import dependence" became a concrete shortage. More than 70 countries restricted exports of medical products, and among them were four of Latin America's top-five suppliers.8 A region that imports the overwhelming majority of its medicine value by definition had no regional fallback: when the suppliers it relied on prioritized their own populations, LAC waited in line. In Manaus, in January 2021, one of Brazil's largest cities ran out of medical oxygen as hospitals overflowed; two months later, the Serum Institute of India halted vaccine exports to protect India's own surge, disrupting supply across the region through the COVAX facility at a stroke.

This is not a museum piece; the shocks keep coming. In 2024, Houthi attacks pushed cargo away from the Suez Canal and around the Cape of Good Hope, adding roughly two weeks to shipping times; in mid-2025, the escalation between the United States, Israel, and Iran threatened shipping through the Strait of Hormuz, through which about a third of the world's seaborne crude passes. Air-cargo rates out of India spiked by as much as 350%, insurance premiums surged, and analysts warned that prices for generics, and even temperature-sensitive cancer drugs flown along those routes, could move within weeks.9

India, the "pharmacy of the world," itself depends on China for roughly 70% of its bulk-drug inputs, and in early 2025 Chinese producers cut key active-ingredient prices by 40 to 50%, a reminder of who sets the terms.9

Nor is the fragility only about distant conflicts: when Hurricane Helene flooded a single North Carolina plant in 2024 that made more than half of the United States' intravenous-fluid bags, American hospitals rationed saline for months, and the United States hit a record 323 active drug shortages early that year.10 Even the wealthiest systems are exposed, which is why both are now treating ingredient dependence as a strategic vulnerability: Washington has moved toward tariffs of up to 100% on branded drugs unless their makers build on US soil, and Brussels has advanced a Critical Medicines Act aimed squarely at reliance on China and India.10 The global pendulum is swinging from lowest-cost sourcing toward "make it closer to home," and Latin America has to decide where it stands in that shift.

The pandemic did not create the dependency; it revealed it, and the years since have kept revealing it. It revealed it precisely where this report locates the gap: in the high-value, complex products and the active ingredients the region does not make for itself. That resolves an apparent paradox the next chapters develop. In a supply shock the region is largely covered on everyday volume and essentials, the pills its own factories already make, but acutely exposed on the narrow, high-value, input-deep slice it does not. The vulnerability is not that the lights go out everywhere; it is that they go out exactly where the most expensive, hardest-to-replace medicines live.

The constructive reading is that each shock also catalyzed a response, and a genuine appetite to invest in production, not only to procure more cleverly. Within a year of the pandemic, the region's institutions had converged on a shared agenda: PAHO launched a Regional Platform to advance manufacturing; ECLAC, on a mandate from all 33 CELAC states, produced a Health Self-Sufficiency Plan; the IDB and CAF began financing the pivot.11 The will and the platform exist. What they need now is evidence on where to direct investment, and the recognition that the region is not one market but several.

The region cannot manage what it does not measure, and that gap is itself a finding

Before the first figure, an admission that doubles as a diagnosis: no standardized, region-wide series exists for how much of each country's medicine demand is met by domestic production. We can measure trade precisely for 28 of 33 countries, but production-volume self-sufficiency is documented in usable form for only the eight-to-ten largest manufacturers. The smaller Caribbean and Central American states publish almost nothing, in part because most are pure beneficiaries of pooled procurement rather than producers, a structural feature of the region, not merely a reporting gap.

This matters because a region cannot steer what it cannot see. The same absence of a shared production-monitoring system that constrains this analysis is precisely what leaves ministries flying blind during a supply shock, unable to know, in real time, which essential medicines depend on a single foreign supplier. Building that visibility, a common dataset on production, capacity, single-source dependencies, and where active ingredients come from, is one of the cheapest and fastest moves available, and a precondition for every recommendation that follows. The first investment a region serious about pharmaceutical security can make is in knowing its own position, quantitatively and continuously. It is a recurring theme of this report that better data is not a footnote to the strategy; it is the first step of it.

The capability map: who builds and who buys, and why only one of 33 has a genuine export edge

When we score all 33 countries on whether they hold a competitive edge in pharmaceutical production, only one clears the bar: the Dominican Republic. A clarification matters here, because the measure is easy to misread. We use revealed comparative advantage, the standard trade metric of whether a country exports more of a product than the world average would predict. It captures export orientation, not manufacturing capability as such.

Brazil, Mexico, Argentina, Colombia, and Chile, the five largest markets, all score below the global average, not because they cannot make medicines (they manifestly can, for tens of millions of their own citizens) but because they make for their home markets and hold almost no export surplus to redirect. That is exactly the point for supply security: a large domestic producer with no exportable cushion cannot easily become a regional supplier of last resort when a neighbour's imports are cut off. And the Dominican Republic's edge is real but narrow: it is a US-facing free-zone cluster that formulates and packages for export to the United States, with most production legally oriented away from the regional market.

Reading the 33 countries by what they produce and what they depend on, we sort them into six profiles using simple rules on trade ratios and revealed advantage, and the profiles have concrete faces. At the top sit four countries with established manufacturing infrastructure, each with a different lesson:

- Brazil makes at scale, but still depends on imported inputs. Its public laboratories and private champions (Eurofarma, EMS, Hypera) produce billions of doses a year; Fiocruz's Bio-Manguinhos supplies yellow-fever vaccine to more than 80 countries, and the Butantan Institute is the region's largest vaccine producer. As of 2026, ANVISA is the only Latin American regulator admitted to the international PIC/S inspection scheme. Yet Brazil imports more than 90% of its active ingredients: world-class assembly built on imported inputs.

- Argentina has unusual market depth and biotech ambition. Nationally-owned firms hold about 70% of the domestic market, and during COVID the biologics maker mAbxience produced the active substance for the AstraZeneca vaccine (the first such product made in the region to support a WHO Emergency Use Listing), while Sinergium Biotech became the region's spoke in the WHO mRNA technology-transfer network.

- Cuba is a biotechnology outlier under economic strain. BioCubaFarma supplies about 60% of the island's essential-medicines list and developed its own COVID vaccines, but chronic shortages show what happens when the technical model outruns the economic base that must sustain it: in late 2024 more than 460 medicines, over 70% of the basic list, were missing or scarce, and Cuba leaned on tonnes of imported Indian active ingredients to keep antibiotic lines running.12 Sophisticated biotech does not substitute for reliable access to basic active ingredients.

- Mexico has market size without manufacturing depth. The second-largest market in the region runs largely on a fill-and-finish model (importing the active ingredient and packaging it into finished doses), importing around 90% of its active ingredients by industry estimates; size and depth are not the same thing.

Below them sit a cluster of export-oriented formulators (Costa Rica, Guatemala, El Salvador, Uruguay) that punch above their size; the five large domestic-market producers just described; seven mid-market importers (Peru, Ecuador, Panama, Honduras, Nicaragua, Paraguay, Bolivia); a tier of Caribbean micro-importers that make essentially nothing; and five countries whose trade data is too thin to place precisely (Cuba sits here on data grounds, though its biotech puts it in a class of its own). Two ambitious newcomers, Colombia's VaxThera and BogotaBio, are building biologics capacity that does not yet exist at full scale, but the direction, and the financing, are real.13

The point of the typology is not to rank winners and losers. It is that these profiles have different needs. A Caribbean micro-importer and an industrial power like Brazil do not face the same problem, and they will not be helped by the same policy. That single insight is what turns a diagnosis into a plan, and it is why the recommendations later in this report are deliberately not one-size-fits-all.

The API blind spot: the region's "manufacturing" is largely the formulation of imported active ingredients

A word on terms, because it is where the confusion usually starts. A medicine has two parts: the active pharmaceutical ingredient (API), the molecule that does the therapeutic work, and the formulation around it that turns the molecule into a swallowable tablet or an injectable vial. Making medicines involves three very different activities: synthesizing the API (the hardest, most capital-intensive step), formulating and packaging it into finished doses (fill-and-finish), and full-cycle manufacturing that integrates both. Most of Latin America operates at the second level. It formulates imported APIs into finished products. Only a few players reach the first.

Brazil is the documented case. It produces only about 5% of the active ingredients its industry consumes, and imports the other ~95%, a striking reversal from roughly 55% domestic production in the 1980s, lost over four decades of de-industrialization.1 And those imports trace overwhelmingly to two origins: China and India together supply just over half of Brazil's API purchases by value (about 55%), and roughly three-quarters of the foreign facilities licensed to export active ingredients to it.14

Across the producer countries we measured, our own basket trace finds the pattern holds: around 59% of active-ingredient imports, by value, come from China and India (an unweighted country average of about 60%), ranging from roughly 40% to 78% by country. That is the concentration of where those ingredients are bought. A separate measure, how much of the input is bought abroad at all, is just as stark: PAHO's 2025 figures put external active-ingredient dependence at about 95% for Brazil and 85% for Argentina, the region's two strongest manufacturers.15

Here a careful reading matters, and it makes the picture worse, not better. The roughly 41% that does not come from China and India is not made in Latin America; it comes overwhelmingly from Europe and the United States. And because trade statistics record a shipment's last point of consignment rather than where its contents were synthesized, active ingredients that reach the region through European distribution hubs (Belgium, the Netherlands, Ireland, Switzerland) are credited to those hubs, not to the Chinese or Indian plants that actually made them, so the China-and-India figure is a conservative floor on the region's true exposure to Asian API production, not a ceiling.

Independent analysis of United States defense procurement finds the same masking at scale: more than half of those medicines were mislabeled as to origin because Chinese and Indian material had been transshipped and repackaged in a third country before delivery.16

The region barely participates in API manufacturing at all, which is why it holds less than 1% of global capacity.3 So the dependency is not "59% on two countries and the rest at home." It is near-total dependence on a handful of extra-regional suppliers, of which China and India are simply the largest and the most concentrated. The most revealing single number is the Dominican Republic's: the one country with a genuine export edge still buys about 53% of its active ingredients from China and India,1 because its competitiveness is the competitiveness of a formulator.

This is the part of the gap that buying smarter cannot fix, and it is where the case for building, selectively, is strongest. It is worth being candid about why the region offshored its API synthesis: Brazil's slide from 55% to 5% was not simply a policy failure but the rational outcome of scale, feedstock, and energy economics that let China and India make most bulk ingredients more cheaply than anyone else.

The case for building is therefore not to compete with Asian API manufacturing across the board, a fight that is lost and not worth re-fighting. It is to pay a deliberate security premium on a short, prioritized list of ingredients where a single-source disruption would be catastrophic and where volumes are small enough that the premium is affordable insurance rather than industrial policy at scale.

One discipline matters in choosing that list: synthesizing an active ingredient still depends on key starting materials (KSMs), the chemical precursors a layer below the API, which are themselves concentrated in China and India, often more tightly than the ingredients they feed. China is estimated to make around 94% of the world's 6-APA, the starting material for amoxicillin.17 This is what supply-chain analysts call the "N-1" problem: apparent diversification at the formulation or even the active-ingredient step is illusory when every supplier draws on a single upstream input. Reshoring the final synthesis step while importing all of its precursors moves the dependency one link upstream rather than removing it, so the list should favour molecules whose precursors the region's own chemical sector can realistically make, or source from more than one country. The goal is to mitigate single-source risk, not to chase outright self-sufficiency.

Argentina has made a start: in 2023 it inaugurated a small public pilot plant for API synthesis at INTI, the country's only public facility of its kind, built to develop and scale a selected set of strategic ingredients (Argentina makes only about 6%, by molecule count, of the roughly 2,000 APIs its industry uses).18

There is a deeper implication that regional plans have largely missed. The region has chemical and petrochemical industries that have rarely been pointed at pharmaceutical-grade synthesis; the active-ingredient gap will not close unless reindustrialization and sovereignty plans deliberately knock on that door, treating the chemical sector as part of the health-security strategy rather than a separate economy. A regional API agenda that ignores the chemical industry is an agenda that ends at the formulation step, which is exactly where the region is already stuck.

The counterintuitive reframe: Latin America imports 91% of its medicine value but only 53% of its kilograms

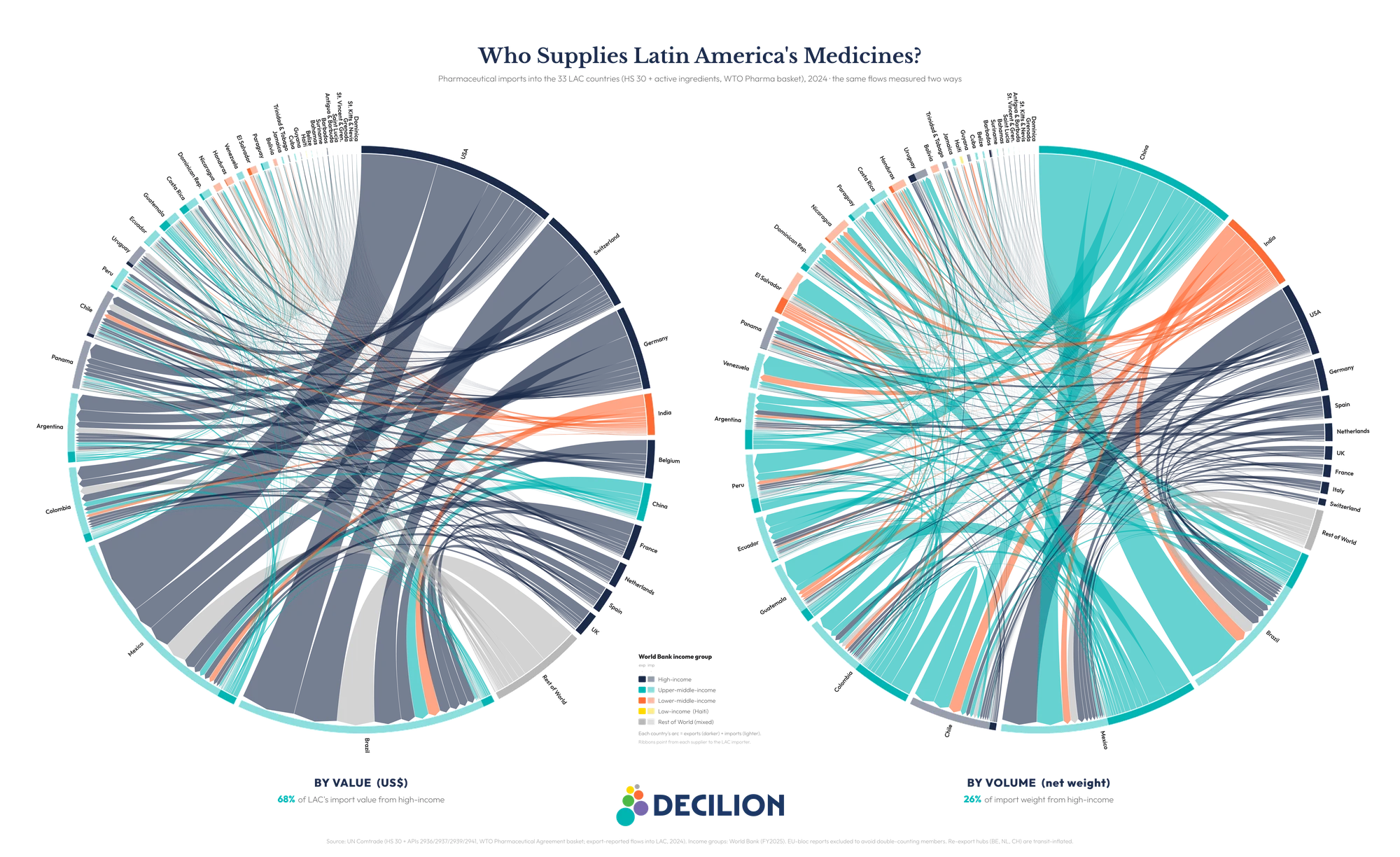

Here is the finding that should reorder the policy conversation. Compare import dependence by dollar value and by physical volume measured in kilograms, and the two numbers diverge sharply. By value, about 91% of the region's finished-medicine imports come from outside LAC. By kilograms, only about 53% do. Nearly half of every kilogram of medicine the region imports already comes from within Latin America and the Caribbean.5

The reason is price density. Extra-regional medicines, the patented, specialty, biologic products from the United States and Europe, cost on the order of US$103 per kilogram at the border. Intra-regional medicines, the generics that move between LAC countries, cost about US$12 per kilogram, roughly a tenth as much.5 The region imports a small volume of very expensive drugs and a large volume of cheaper ones, and the expensive ones come from outside.

The same divergence has a geography. The roughly 91% of medicine value that arrives from outside the region is not one bloc: by value, it is overwhelmingly high-income, the United States, Germany, Switzerland and the rest of Western Europe supplying about two-thirds of all the region's imports. By weight, those same economies account for only about a quarter, as China and India, the generics and active-ingredient producers, take over, alongside the large flow of trade within the region itself. (The chord below draws on a slightly broader, export-reported 2024 basket that also counts active ingredients; because those are heavy, low-cost flows from China and India, the chord's intra-regional share of weight runs below the finished-medicine figure above. The value-and-weight pattern is the same.)

National data confirms what the trade decomposition implies: the region's own factories already supply the majority of the medicine its people physically consume. Domestic industry covers a confirmed 73% of Brazil's finished-medicine volume (industry sources put it as high as 80%), roughly 80% of Colombia's, about 70% of Argentina's (by both value and units, per the national industry chamber), and around 60% of Cuba's essential-medicines list.4 By the measure that matters for everyday access, pills on shelves, much of the region is already substantially self-sufficient.

This reframes the problem in a more hopeful direction. The region does not face a wholesale manufacturing collapse; it faces a concentrated, high-value, input-deep gap. But that high-value gap is not one problem with one answer, and being honest about the difference is what keeps the report's title from over-promising. It divides cleanly in two.

The first slice is patented, on-patent specialty drugs, the biologics and oncology and metabolic therapies under exclusivity. A region cannot simply "make" these regardless of how much capacity it builds: they are a question of price and access. The most powerful lever here is pooled negotiation and procurement, which can move prices across a whole basket of drugs at once and with relatively little friction. Intellectual-property flexibilities (voluntary or compulsory licensing, and the IP-flexibility line written into the ECLAC/CELAC plan)19 are entirely legitimate, legal, and available to any country or civil-society organization that chooses to pursue them; but in practice they tend to work one drug at a time and require sustained political and diplomatic effort, so they are best understood as a complement, used when warranted, rather than the region's main route to affordability.

The second slice is off-patent complex products, biosimilars (lower-cost follow-on versions of biologic drugs once their patents lapse), and active ingredients, where exclusivity is not the barrier and the answer genuinely is to build, selectively and regionally. "Make the medicine" applies in full to the second slice; for the first, the lever is to afford and access it, not to manufacture around a valid patent. Sorting the gap this way turns "buy versus build" into the sharper "buy, build, or license."

Integration is real for lower-cost volume and thin where the value is: intra-regional trade is 47% of LAC's imported kilograms but just 9% of its value

If the region already moves nearly half its imported kilograms across its own borders, why does it capture so little of the value? Because intra-regional trade is concentrated exactly where margins are thin. Latin American and Caribbean countries trade generics with each other readily (Mexico supplies Central America, Colombia the Andean market, Argentina and Uruguay the Southern Cone), but the high-value patented drugs and biologics that drive the import bill flow in from outside almost entirely. The arithmetic is blunt: intra-LAC trade is about 47% of the region's imported medicine kilograms but only about 9% of its value.5

The export side tells the same story from the other direction. Across the 28 reporting countries, LAC exported only about US$7.5 billion of finished medicines in 2024 against roughly US$40.2 billion of imports, a deficit on the order of US$32.7 billion, with imports running more than five times exports.20 Not one LAC country runs a pharmaceutical trade surplus. Mexico and Brazil are the largest exporters, and much of what the region does export stays within the region, the generics that move between neighbours. But the totals are small, and on active ingredients they are negligible. The region sells the world very little, and what little it sells is low-value.

That is an opportunity, not just a gap. A region that already trades half its imported volume internally has a foundation to build on: deepening intra-regional generic trade, buying more from neighbours instead of from outside, is a lever available today, with the plumbing already in place. One caveat on sequencing: in the short term that extra depth has to come from the export-oriented formulators (Costa Rica, El Salvador, Guatemala, Uruguay) that already hold a surplus to sell, because the large domestic producers run mostly at capacity for their own people and have little to redirect; their contribution to regional supply is a medium-term goal that depends on the financing to scale.

And it points to where new capacity would matter most, not in duplicating the generic plants that already feed regional trade, but in the higher-value and active-ingredient segments where the region trades almost nothing with itself. The integration that exists shows the integration that is missing, and where to aim.

The region is already piloting the pieces of the answer, from joint procurement to public ingredient plants and regional vaccine hubs

None of the levers this report recommends is hypothetical. Each is already operating somewhere in the region; the opportunity is to do them deliberately, at scale, and matched to the right countries.

Pooled procurement, where it fits. For the smaller and mid-tier economies, whose challenge is buying essentials affordably, joint purchasing already works well. Central America's COMISCA mechanism has negotiated medicines collectively for more than a decade, saving its members on the order of US$210 million and cutting prices by 30–60% across a wide basket of products; the eastern Caribbean's pooled procurement service has trimmed costs by around 20% since the 1980s.6

PAHO's Strategic and Revolving Funds anchor this layer for the whole region, and they serve every country, the largest included, which use them and benefit from them. The point is one of scope, not of exclusion: these mechanisms are strongest for essential and standardized medicines and for the systems that most need help buying them, and they have begun reaching into some higher-cost products. What they were not built to carry at scale is the intellectual-property leverage and the health-technology-assessment muscle the largest economies need to negotiate patented, complex specialty drugs. Those economies need additional mechanisms to complement PAHO, not a smaller role for it.

And pooled demand can do more than save money; it can pull production into the region. PAHO reports that regional manufacturers supplied about 25% of its influenza-vaccine demand in 2025, with agreements to lift that toward 65% from 2026, a concrete demonstration of what happens when a guaranteed regional market is linked to regional capacity.15

Strategic production, selectively. On the building side, the region has begun to target rather than sprawl, and the 2024 to 2026 pipeline is real. Argentina's public API pilot plant at INTI is one example; Brazil's industrial-health complex uses technology-transfer partnerships to localize strategic products, and its public producer Hemobrás is building toward covering the national health system's full demand for hemophilia treatment.18 More recent moves point upstream, toward API synthesis and the high-value segments the region has lacked: Mexico attracted a roughly US$2 billion Canadian-backed active-ingredient plant in Hidalgo in 2026 and a wave of investment including local insulin production, and Colombia's public University of Antioquia plant began industrial production of an essential antimalarial in 2026, its first lot more than a million tablets.21

These templates should be read honestly. Argentina's plant is pilot-scale; Hemobrás has faced delays and still imports part of its input; and announced plants do not always materialize, as Chile's long-stalled Sinovac vaccine facility shows, held up while the manufacturer sought guaranteed demand.21 But the unevenness proves the targeting logic rather than refuting it: picking a strategic few, guaranteeing them a market, and building them is sound even where execution has lagged. That is the model to scale, with realistic timelines and demand commitments attached.

One design choice decides whether these plants buy autonomy or merely relocate it: who supplies their inputs, equipment, and standards. A facility built and fed on imported active ingredients moves the assembly step without moving the dependence, the very trap China extends abroad when it finances pharmaceutical plants through its Belt and Road Initiative, embedding its own key starting materials, equipment, and technical standards in the host country.22 That the Hidalgo plant is Canadian-backed is a reminder that the region can choose its partners; the discipline is to build with diversified, ideally regional, inputs rather than to reproduce the single-source problem one tier down.

Regional production of complex products. For the most advanced segment, PAHO selected two hubs, Bio-Manguinhos/Fiocruz in Brazil and Sinergium Biotech in Argentina, to develop and produce mRNA vaccines for the whole region, with technology transfer built in.11 It is the clearest existing template for the principle that complex capacity should be built once, shared regionally, and aimed at products the region cannot afford to keep importing. The pieces exist. What is missing is the connective strategy that treats them as a portfolio rather than a scatter of national experiments.

The cost of inaction: on the current path dependence stays stuck near 94–96% through 2035, when coordination could instead repatriate 19–32 points of the prize

What happens if the region does nothing differently? Our scenario model, illustrative and bounded rather than a forecast, projects extra-regional dependence forward under three paths.7 On the status quo, with 33 countries pursuing separate national plans and no coordinated demand, dependence stays roughly flat, hovering near 94–96% by 2035, as demand for high-value imported drugs grows about as fast as local capacity. Standing still does not self-correct: the gap does not close on its own, and the most exposed segment quietly grows.

Two coordinated paths bend the curve the other way. Under subregional coordination, blocs pooling demand and selectively producing, dependence falls toward roughly 77%. Under full regional integration, harmonized regulation, a shared strategic-production agenda, and demand routed to regional suppliers, it falls toward roughly 64%. The gap between drift and action is the prize: 19 to 32 percentage points of dependence repatriated. Applied to the region's roughly US$40-billion-a-year import base, that is on the order of US$8–13 billion a year of medicine supply shifted from outside the region to within it, a meaningful share of the roughly US$33 billion dependency, though not the whole of it.

The caveat is that these are modeled scenarios resting on stated assumptions, not promises. The annual rates that bend each curve are expert-judgment placeholders pending calibration against the region's own track record, not estimates fitted to historical data; they convey the shape of three choices, not point predictions.

One caution in particular: the price savings documented above (COMISCA, the eastern Caribbean) measure cheaper purchasing, which is not the same as a smaller extra-regional share, so the realized-savings evidence underwrites the plausibility of coordination rather than the exact reduction in dependence. There is also a political caveat the numbers cannot capture: the region has repeatedly stood up regional health bodies that then stalled (UNASUR's health council, AMLAC, the CELAC plan now four years in), so capturing even the lower, subregional path depends on sustaining a cooperation the region has rarely held for a decade. What is robust is the direction, and the fact that the mechanisms are the proven ones already operating in the region.

Stakeholder playbooks: who moves first, and on what, because the region is not one market but several

Because the region's profiles differ, the moves differ. The following are deliberately not a single regional plan but coordinated ones, matched to who is exposed to what.

Ministries and regulators: start with what you can do alone, then differentiate by profile. The single no-regrets move, available to any ministry this quarter with no treaty and no coalition, is to build the shared production-and-dependency dataset this report keeps returning to. A ministry cannot steer, or defend in a shortage, what it cannot see; knowing which essential medicines hang on a single foreign supplier is the cheapest insurance available.

From there the strategy splits by profile. For smaller and mid-tier economies, the fastest gains come from deepening pooled procurement of essentials through PAHO and subregional blocs. For the largest economies, which already supply their own essentials, the priority is a dedicated mechanism beyond PAHO for the high-cost, complex drugs that drive their exposure.

That last point runs into a genuine, unresolved limitation. Latin America and the Caribbean has no single economic-integration vehicle of the kind the European Union or the African Union give their members; the Organization of American States relies heavily on PAHO for health, and sub-regional blocs reach only their own members. MERCOSUR has run a joint high-cost-drug price negotiation since 2015, its first round cutting the price of an antiretroviral,23 but it stops at MERCOSUR's borders. There is no region-wide high-cost-drug mechanism yet, and creating one is unfinished business with no settled answer.

The realistic path is not to wait for a continental institution that may never come, but to start small: a willing coalition of a few larger economies, convened through a forum like CELAC, the one space that gathers all 33, pooling demand for a short list of high-cost drugs, proving the savings, and growing from a demonstrated base. For the fragile or sanctioned states (Cuba, Venezuela, Haiti), where coalition politics and sanctions complicate any new vehicle, PAHO's funds often remain the only neutral channel and should stay that backstop.

Underpinning all of it is regulatory convergence, the precondition that lets a regional market function and lets a supplier approved in one country bid in another.19 That convergence is unfinished and contested: the region's own AMLAC initiative remains largely declaratory, even as Africa, often cast as the laggard, moved its new Medicines Agency from treaty to a Kigali headquarters in 2025 with more than 30 countries ratifying.

But ministries need not wait for a new treaty to get mutual recognition: PAHO already designates a network of national regulators of regional reference (among them Brazil's ANVISA, Argentina's ANMAT, Mexico's COFEPRIS, and Colombia's INVIMA), and any government can pass a domestic fast-track decree that automatically accepts a registration cleared by one of them. That is mutual recognition available now, country by country, without a continental institution.

The clock is not neutral, either: the EU-Mercosur agreement reached in December 2024 will eventually cut tariffs on European medicines entering the bloc, easing prices for buyers but raising competitive pressure on nascent producers unless industrial policy moves in step. That pressure is specific to the Southern Cone, though; much of the rest of the region (Mexico, Central America, the Andean countries) has imported European and US medicines at or near zero tariff for years under existing trade deals, so the MERCOSUR transition is best watched as a test case for how regional industrial policy adapts.24

Payers and providers: make the region biddable, and buy with supply security in mind. Much of the value gap can be narrowed by sourcing more of the generic basket from regional manufacturers that already exist. But procurement law across most of the region mandates open competitive tender, and trade commitments (including the EU-Mercosur deal) limit explicit buy-local clauses, so the lever is not preference by fiat.

It is to make regional suppliers able to compete: mutual recognition of approvals so a drug cleared in one country can bid in another, joint cross-border framework tenders that aggregate demand, and award criteria that price in supply security rather than the lowest sticker price alone. For the high-value products where the gap truly bites, channel procurement to the mechanism that fits the country's profile: subregional pooling for the smaller systems, and, for the larger economies, the high-cost coalition they will need to build.

Pharma, life-sciences, and the chemical sector: invest where the region cannot keep importing. The commercial opportunity is not greenfield generics, where the region is already competitive, but the segments it is missing: a prioritized set of strategic active ingredients and complex, higher-value products. This is also a call on an industry the health conversation usually ignores. Active-ingredient synthesis is a chemical-industrial capability, and the region's chemical and petrochemical firms, not only its drug makers, are the ones positioned to build it.

The firms, in either sector, that build for regional demand rather than only national markets will find both a market and a concrete policy tailwind: guaranteed regional offtake at a security premium for a named short list of strategic ingredients, plus the development-bank de-risking described below. The premium is a deliberate budget choice, paying a little more on a narrow list to insure against catastrophic single-source shocks, and it coexists with pooled procurement's pay-less logic on the much larger essentials basket; the two are not in tension because they apply to different products.

Development banks (IDB and CAF): finance the build, and de-risk the demand. The investable object is the differentiated regional portfolio, but it has to be financed through real instruments. Banks finance the build (plant and shared active-ingredient capex, the regulatory-capacity and data infrastructure) through IDB Invest and CAF debt and equity into formulators and chemical firms, and through grant-funded technical assistance for the shared dataset and regulatory convergence. Just as important, they de-risk the demand: advance-purchase commitments and volume guarantees that turn a security premium into a bankable offtake. The binding constraint is rarely the loan; it is a credible, multi-year demand commitment, which is why the demand-side levers (pooled procurement, supply-security award criteria) and the finance have to move together.

The region is not financing this alone, either. As Washington looks to "friendshore" pharmaceutical inputs away from China, US development finance has begun eyeing Latin America explicitly: a 2025 Council on Foreign Relations analysis names Argentina, Brazil, and Mexico as candidates for active-ingredient capacity backed by US International Development Finance Corporation lending, and cites Brazil's 2019 move to set separate regulatory standards for bovine and porcine heparin as proof that such sourcing barriers are manageable regulatory problems rather than market ones.25

That external capital is an opportunity to take up on the region's own terms, not a substitute for a regional strategy. The 19-to-32-point repatriation is the return; financing 33 redundant national factories would not earn it, financing a coordinated few aimed at strategic gaps would.

Methodology and limitations: what our dependency numbers can and cannot bear

Our trade figures come from United Nations Comtrade, for the latest available year (2024, with 2023 used where 2024 is not yet complete). We measure extra-regional dependence by summing each country's imports from all of its LAC partners against its world total, by both value and net weight in kilograms, an all-partner method rather than a top-handful approximation.

The headline is built from the bottom up, not extrapolated. The ten largest markets, which hold about 80% of regional import value, source roughly US$29 billion of their medicine from outside the region when measured directly; adding conservative shares for the smaller reporters brings the total to about US$32 to 34 billion, and the five non-reporting countries add only around US$0.3 billion more. We anchor on about US$33 billion as a lower bound. The 91% value-share and the 53% kilogram-share are computed over those ten largest markets.

A few limits matter. Trade is not production: on its own it cannot separate domestic manufacturing from imports for domestic use, so we triangulate with national-regulator production data where it exists, which is only eight to ten of the 33 countries. Net weight in kilograms is a proxy for physical volume, not for doses. The active-ingredient analysis uses the EFPIA-curated tariff basket, a proxy that includes some non-pharmaceutical uses of the same headings. The 2035 paths are a transparent, bounded scenario model, not a forecast, and the market-size and active-ingredient-capacity figures are third-party estimates, cited as such. The full method, and a script that recomputes the headline from the trade data, are published at the GitHub repository linked below. None of these caveats changes the central finding.

Suggested citation: García Ruiz, J. (2026). Made in the Region, Up to a Point: Pharmaceutical Supply Security in Latin America and the Caribbean. Decilion Insights. decilion.com/insights/drug-manufacturing-lac.

Declaration of interests: the author declares no competing interests.

Data sharing: the calculation script and the trade table behind the report's signature value-vs-weight finding are published openly at github.com/Decilion/decilion-insights (reproduce.py recomputes the figures); the full datasets and analytical models are available from Decilion on request.

This is an independent Decilion Insights report, analytical grey literature, not peer-reviewed; its authority rests on transparent methods and reproducible data rather than external review. ORCID 0000-0002-7179-128X.

- API ~59% China+India: Decilion analysis of UN Comtrade trade data (EFPIA active-ingredient basket), 2024 (value-weighted 58.6%, unweighted ~60.3%). Brazil ~5% domestic API / ~90–95% imported (SciELO, An. Acad. Bras. Ciênc. 2023, citing ABIQUIFI/ANVISA 2020). The "~55% in the 1980s" is secondary (Abiquifi via Chaves2021/IPEA), retained as widely-cited but not primary-confirmed.

- Global pharmaceutical market ~US$1.7 trillion (2024); United States ~53% of the global market; LAC ~US$92bn ≈ ~5% (Statista; Towards Healthcare, Latin America pharmaceutical market 2024 ≈ US$91.85bn). LAC ~8% of world population (UN/World Bank). Market-size definitions vary (sales vs. revenue); figures are order-of-magnitude and cited as third-party market research.

- India and China together account for roughly two-thirds of global API manufacturing (Statista, 2023: "almost two thirds of all active pharmaceutical ingredients manufactured worldwide came from China and India"; corroborated by U.S. Pharmacopeia, Quality Matters, "Global manufacturing capacity for APIs remains concentrated," qualitymatters.usp.org). LAC's own API production is well under ~1% of the global total: an order-of-magnitude figure (LAC is only ~7% of global API consumption yet imports the overwhelming majority of what it uses, with PAHO 2025 putting external API dependence at ~95% for Brazil and ~85% for Argentina, its two largest producers; consistent with the IDB pharmaceutical GVC study, ref 5).

- Brazil ~73.2% domestic (2019), IBGE Conta-Satélite de Saúde. Colombia ~80% (2024, from 69% in 2018), ANDI. Argentina ~70%, CILFA 2022 ("La industria farmacéutica argentina," cilfa.org.ar): nationally-owned labs = 70.8% by value, 70.3% by units. Cuba ~60%, BioCubaFarma supplies 60% (369 of 627) of the cuadro básico (Granma/Cubadebate, 2022).

- Decilion analysis of UN Comtrade bilateral trade data for the 10 largest markets (2024), summed by partner and 6-digit code: extra-regional value-share 90.9%, net-weight share 53.0% (intra 47.0%), unit values US$103/kg extra vs US$11.6/kg intra (8.8×), net-weight coverage 98.5%. Reproducible from the published trade table and script at github.com/Decilion/decilion-insights. National volume shares per reference 4.

- COMISCA US$209.8M cumulative since 2009 and 30–60% reductions (SE-COMISCA portal). OECS −20%, OECS Pharmaceutical Procurement Service has cut the regional market cost of medicines ~20% since 1986, saving ~US$4M/yr (oecs.int). ARV −97% (Lal2022) retained from peer-reviewed; confirm at primary if quoted prominently.

- Decilion scenario model (illustrative, bounded): extra-regional dependence baseline ~94% (2024; the measured all-partner value-share over the 10 largest markets is ~90.9%; the modelling baseline is set slightly higher, not lower, on the judgment that the more-dependent non-reporting countries and indirect or repackaged imports add to the extra-regional share, and the choice sits well inside the model's ±8% band), three named scenarios to 2035 (status quo +0.2%/yr → ~96%; subregional blocs −1.8%/yr → ~77%; full integration −3.5%/yr → ~64%), ±8% band clamped to [0,100]. The annual rates are expert-judgment placeholders pending calibration, not estimates fitted to historical data. Documented pooled-procurement price savings measure cheaper purchasing, distinct from a reduced extra-regional share. Repatriable value ≈ 19–32 points × ~US$40.2bn import base ≈ US$8–13bn/yr. Illustrative; NOT a forecast.

- ECLAC, "Las restricciones a la exportación de productos médicos…" (May 2020, doc S2000309, repositorio.cepal.org): more than 70 countries, including four of the five main suppliers to the region (led by the United States), restricted exports of medical products in response to COVID-19. Manaus oxygen crisis (Jan 2021) and Serum Institute export halt (Mar 2021) widely reported and confirmed.

- 2024 Red Sea/Houthi disruption rerouted cargo around the Cape of Good Hope (~10–14 extra days; NHS Supply Chain, 2024); 2025 US-Israel-Iran escalation and Strait of Hormuz threat (the IEA estimates ~34% of seaborne crude transits Hormuz). India air-cargo rates rose by as much as ~350%, insurance premiums surged, and analysts warned of price moves for generics and temperature-sensitive cancer drugs flown along those routes within weeks (The Hill; Think Global Health; Reuters via Investing.com, Apr 2026; BioProcess International). India depends on China for ~70% of bulk-drug inputs; Chinese producers cut key API prices ~40–50% from Feb 2025 (industry trade press; CNBC, "Strait of Hormuz standoff puts supply of America's generic drug prescriptions at risk"; ORF; Maritime Gateway), consistent with the ~350% air-cargo figure used here. News-sourced illustrative context, not a Decilion computation.

- US hit a record 323 active drug shortages in Q1 2024, the highest since ASHP began tracking in 2001 (ASHP; AHA News, 12 Apr 2024). Hurricane Helene (Sept 2024) flooded Baxter's North Cove, NC plant, which made about 60% (~1.5M bags/day) of US intravenous-fluid supply, triggering a national saline shortage (American Hospital Association; FDA). The US moved toward tariffs of up to 100% on branded/patented drugs unless made on US soil (announced 25 Sep 2025; formal proclamation 2 Apr 2026; White House fact sheet; CNBC); the EU advanced a Critical Medicines Act targeting China/India ingredient dependence (proposed Mar 2025; Council position Dec 2025; Consilium). ~33.7% of US generic APIs (2020–21) were made at a single facility (Health Affairs, Socal et al., 2022, doi:10.1377/hlthaff.2022.01120).

- PAHO CD59/8 + Resolution CD59.R3 (59th Directing Council, Sept 2021) + Regional Platform / Special Program on Regional Production (paho.org). PAHO mRNA hubs (Bio-Manguinhos/Fiocruz, Sinergium Biotech) per PAHO/WHO. IDB GVC study (DOI 10.18235/0013712, 2025); CAF financing role from secondary.

- Cuba, late 2024, had 460+ essential medicines missing or in low coverage (over 70% of the basic list) (official data via CiberCuba, 18 Dec 2024); BioCubaFarma received ~60 tonnes of Indian pharmaceutical ingredients (a donation) to sustain antibiotic production for 6–12 months (CiberCuba, 9 Aug 2024).

- BioCubaFarma supplies ~60% (369 of 627) of Cuba's cuadro básico de medicamentos and produces indigenous vaccines (Granma/Cubadebate, 2022; BioCubaFarma_Nature2020). Brazil/Argentina/Mexico/Colombia company profiles (Eurofarma/EMS/Hypera, mAbxience/Sinergium, VaxThera/BogotaBio) from the prior Decilion research package.

- (ANVISA via SciELO 2023): ~78% of facilities abroad that export APIs to Brazil are in China and India. The ~55% by value is the Decilion EFPIA-basket analysis of UN Comtrade (Brazil = 54.8%; A secondary report, CNN Brasil/ANVISA, gives India ~37% / China ~35% by value; not primary-confirmed.).

- PAHO Annual Report 2025 (paho.org/pub/en/annual-report-2025) external active-ingredient dependence ~85% (Argentina) and ~95% (Brazil); the Regional Revolving Funds procured ~25% of influenza-vaccine demand from regional manufacturers in 2025, with agreements to supply up to ~65% from 2026; 30+ vaccine-value-chain facilities across seven LAC countries.

- (CFR, "The Pharma Choke Point," 2025): "54 percent of DOD-sourced national drug code (NDC) medicines were noncompliant with the Trade Agreement Act, actually derived from China, India, or unknown origins via transshipment and repackaging." Cited as external corroboration that trade "origin" (last consignment) understates true China/India manufacturing origin.

- China ~94% of global 6-APA (amoxicillin's key starting material), and the broader concentration of key starting materials (KSMs) one tier below APIs. (Council on Foreign Relations, "The Pharma Choke Point," 2025, cfr.org/reports/the-pharma-choke-point): "China controls the raw or key starting materials for 94 percent of amoxicillin"; "five Chinese companies… control over four-fifths of global 6-APA production." Independently corroborated by CNN Business (3 Jun 2025). The "N-1 problem" (downstream diversification masking a single-source upstream input) is that report's framing.

- Argentina public API pilot plant at INTI (argentina.gob.ar): inaugurated 2023, ~US$2.5M, GMP up to 160 L, ANMAT-enabled; the country's only public API facility; develops/scales selected APIs (incl. TB/Chagas). Argentina makes ~6% of its ~2,000 APIs locally. Brazil Hemobrás (recombinant Factor VIII, Goiana/PE) (Ministério da Saúde / Agência Gov, 2024): targeted to meet 100% of SUS hemophilia demand from 2025, production ramping (packaging 19%→62% of batches).

- ECLAC/CELAC Plan for Self-Sufficiency in Health, unanimously approved by all 33 CELAC states at the 6th Summit, Mexico City, 18 Sept 2021; seven lines of action (pooled procurement; public procurement for regional markets; vaccine consortia; regional clinical-trials platform; IP flexibilities; regulatory convergence; primary-health strengthening).

- Decilion analysis of UN Comtrade trade data (HS Chapter 30), 2024: across 28 reporting LAC countries, HS30 finished-medicine exports ≈ US$7.5bn vs imports ≈ US$40.2bn in 2024 → deficit ≈ US$32.7bn; imports ≈ 5.3× exports. No LAC country runs a pharmaceutical trade surplus. Top exporters: Mexico (~US$2.7bn), Brazil (~US$1.2bn), Argentina (~US$0.9bn). Intra-regional share of exports is qualitative here; partner-level export breakdown not yet pulled.

- Recent LAC manufacturing pipeline (2024–2026): Mexico, ~US$2bn Canadian-backed (Solar International Core Canada) API plant in Hidalgo (MOU; ~US$70m initial land outlay) plus a broader pharma-investment wave incl. local insulin (Globe and Mail; Mexico Business News, May 2026); Colombia, University of Antioquia public plant began industrial antimalarial (chloroquine) production, first lot ~1.7M tablets (Infobae; Colombia One, May 2026); Argentina, PAHO/Pfizer/Sinergium local PCV20 pneumococcal production, first doses expected 2026 (PAHO; Sinergium Biotech, Jan 2025); Chile, Sinovac vaccine plant stalled pending a long-term demand/tender guarantee (La Tercera, 2025).

- (CFR, "The Pharma Choke Point," 2025): "By embedding Chinese-origin APIs, key starting materials, equipment, financing, and technical standards into pharmaceutical manufacturing across developing countries, the BRI extends China's sway globally," extending dependence even where direct exports are limited.

- MERCOSUR and Associated States established a joint mechanism to negotiate/purchase high-cost medicines with PAHO support, concretized November 2015 (paho.org; mercosur.int; argentina.gob.ar); the first joint negotiation covered the antiretroviral Darunavir via PAHO's Strategic Fund, and the bloc has since advanced toward a consolidated high-cost-drug purchasing platform for a market of 300M+ (Prensa Mercosur, May 2026). Named here as the existing precedent to scale; the choice of vehicle remains a strategic call.

- AMLAC (Agencia de Medicamentos de Latinoamérica y el Caribe, Declaration of Acapulco signed 26 Apr 2023 by Mexico, Cuba and Colombia) remains largely declaratory/not operational (gob.mx/COFEPRIS; GaBI Online, 2023). African Medicines Agency: Kigali headquarters inaugurated November 2024 (its first Director-General was appointed June 2025); 31 ratifications by Dec 2025 (Xinhua/African Union; AMA). EU-Mercosur political agreement reached 6 Dec 2024. MERCOSUR applies among the region's highest pharmaceutical tariffs: the WTO MFN applied simple average on HS 30 is about 6.8% (Brazil), 7.2% (Argentina), 6.7% (Paraguay) and 7.9% (Uruguay), with individual lines up to ~35%; by contrast the Dominican Republic is at 0% and most of Central America and the Caribbean at or near zero (WTO Stats, latest available year, accessed via Decilion's pharmaceutical-trade tooling). MERCOSUR revived a regional high-cost-drug public-procurement discussion (Prensa Mercosur, May 2026).

- (CFR, "The Pharma Choke Point," 2025): "Geographic diversification of the U.S. supply chain should explore friendshoring partnerships with Argentina, Brazil, and Mexico"; the DFC and the Export-Import Bank "should extend low-interest financing to projects that build API and KSM capacity in lower-cost allied nations"; and Brazil's 2019 separate porcine/bovine heparin standards "demonstrate that this is a manageable regulatory problem.".