When the world's supply chains seized in 2020, Latin America and the Caribbean found it had no regional fallback, and waited in line. More than seventy countries restricted medical exports, four of them among the region's top five suppliers. The lesson almost everyone drew was that the region cannot make its own medicines. The trade data says something more useful, and more hopeful, and getting the diagnosis right changes what the region should build next.

The warning keeps arriving in new envelopes. When the Strait of Hormuz looked like it might close in 2025, air-cargo rates out of India, the "pharmacy of the world," jumped by as much as 350%. When a hurricane flooded a single North Carolina plant in 2024, more than half of the United States' intravenous-fluid supply went with it. So you would expect the numbers to show a region helpless to supply itself. They do not, and that is the part worth rethinking.

The region already makes most of its medicine

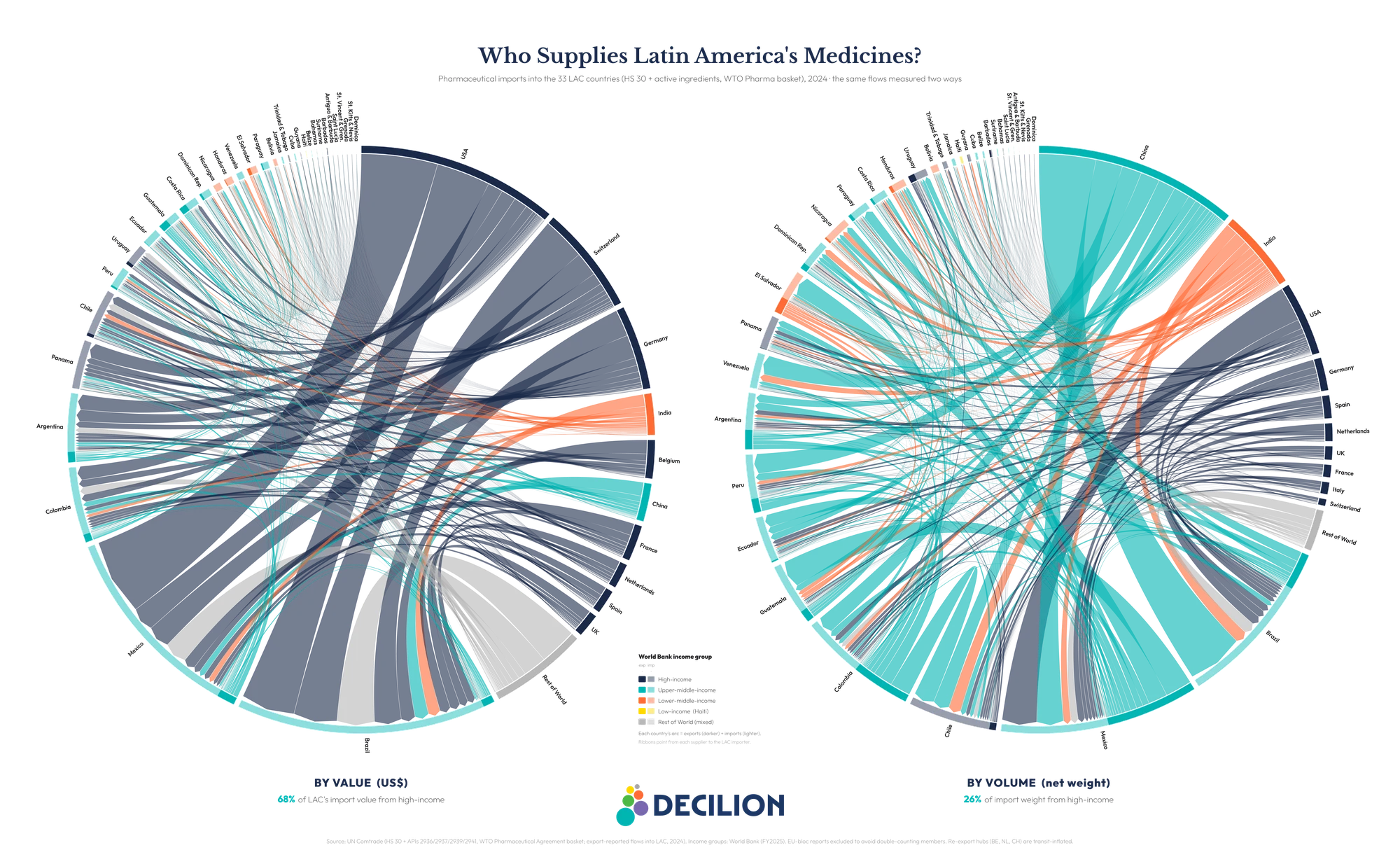

Measure the dependency directly, by money and by kilograms, and the usual story reorders itself. By value, about 91% of the region's finished-medicine imports come from outside the region. By kilograms, only about 53% do. Nearly half of every kilogram of medicine the region brings in already comes from a neighbour. The reason is price density: the medicines that arrive from the United States and Europe cost roughly US$103 a kilogram, while the generics that move between Latin American countries cost about US$12. The region already makes the everyday volume. What it imports is the expensive, complex, patented slice, which is exactly the part that vanishes first in a crisis. That gap is worth on the order of US$33 billion a year.

Who supplies Latin America's medicines, 2024. By value (left), a handful of high-income countries dominate; by weight (right), China, India and the region's own neighbours carry the load. The same split this piece describes, drawn country by country. Full method and data in the report. Chart: Decilion. Data: UN Comtrade 2024.

This is a better problem to have than the one we thought we had. It is narrow and specific, and it points at something the region can actually build.

The real gap is active ingredients, not the pill

A medicine is only as domestically made as its active ingredient, the molecule that actually does the work, and there the region barely participates. It holds under 1% of global active-ingredient capacity. Brazil, its largest producer, makes about 5% of its own active ingredients, down from roughly 55% in the 1980s. About 59% of the region's active-ingredient imports come from China and India, and almost all the rest from Europe and the United States, not from home.

The dependency runs one layer deeper still. Synthesising an ingredient depends on key starting materials, the chemical precursors a tier below it, and those are concentrated even more tightly: China is estimated to make around 94% of the world's 6-APA, the starting material for amoxicillin. Reshoring the final step while importing every precursor does not remove the dependency; it moves it one link upstream. Which is the whole point of the title. Making the pill, formulating and packaging a finished medicine, is the step the region has largely mastered. Making the medicine, building some control over API synthesis, is the step it has not. Medicine security needs an industrial strategy, not only a health-sector plan.

The answer is not 33 national factories

Naming the gap precisely also rules out the two reflexes it usually triggers. The answer is not for every country to build everything, and it is not to shrug and keep buying. It is more interesting than either, and the region is already piloting the pieces of it.

Central America's pooled-procurement mechanism has bought medicines collectively for over a decade, saving its members hundreds of millions of dollars and cutting prices across a wide basket. Argentina has opened a small public plant to synthesise strategic active ingredients. Brazil and Argentina host regional hubs being built to develop and produce complex vaccines for the whole region, technology transfer included. None of this is hypothetical; all of it already exists. The opportunity is to do these things on purpose, matched to each country's actual capability, and together: pay a deliberate security premium on a short list of ingredients where a single-source shock would be catastrophic, and pool demand on the much larger essentials basket where the logic is simply to pay less. The two are not in tension, because they apply to different products.

The unfinished business

There is a harder truth underneath the optimism. The region has the tools, the factories, and now the diagnosis, but it has no single vehicle to organise any of this at regional scale yet, and building one is unfinished business. That is a choice in front of governments, payers, development banks, and the chemical industry the health conversation usually forgets to invite, not a fate handed to them by geography.

The region can make the pill. Whether it decides to make the medicine, by building the strategic few active ingredients it cannot afford to keep importing, is the choice in front of it now.

Our full report maps the manufacturing capability of all 33 countries, digs into the active-ingredient blind spot and what to do about it, and estimates what coordination could actually repatriate by 2035.

Read the full Decilion report

Made in the Region, Up to a Point: Pharmaceutical Supply Security in Latin America and the Caribbean. The data-driven companion to this op-ed, with the full country-by-country capability map, the active-ingredient analysis, and the 2035 scenarios.

Read the report →